Value Without Risk? Wouldn’t That Be Nice — Why Agile Is Risk-Driven Development

Potential value and risk are correlated almost everywhere — in investing, in careers, in product development. You cannot eliminate the risk that comes with real value. But you can de-risk it efficiently, and that is what agile is actually for.

Click image to open full size

Click image to open full size Why Agile is Actually Risk-Driven Development (RDD)

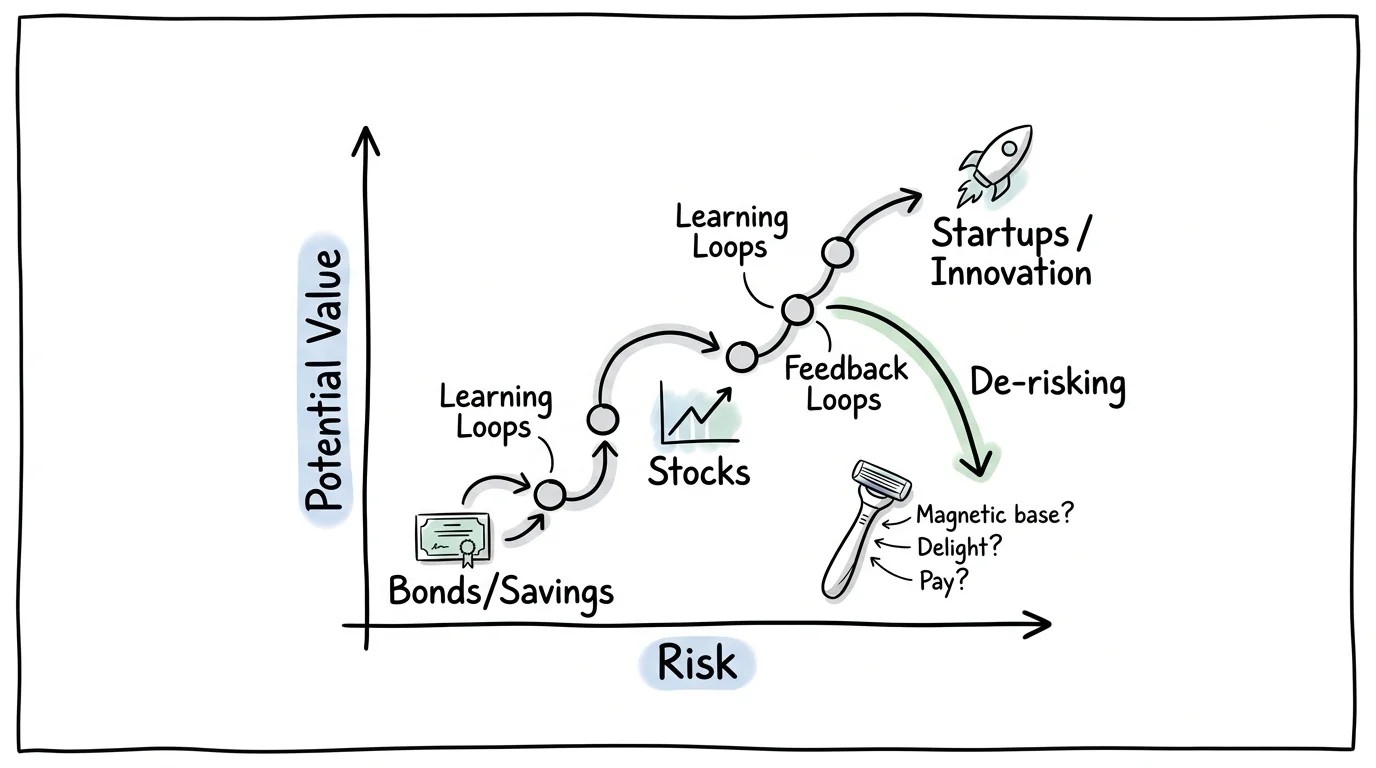

Wouldn’t it be nice to create outsized results without taking any risk? It would — and it is not how the world works. Look at almost any domain and you find the same correlation: the higher the potential value, the higher the risk that comes with it. Bonds are safe and grow slowly; a single concentrated stock can soar or crater. A corporate job is lower-risk and lower-upside than founding a startup. A me-too product is safe and unremarkable; a genuinely differentiated value proposition carries real risk. Investors call the excess return alpha, and alpha always comes bundled with risk.

The good news is that, unlike a stock pick, product and business risk is not fixed. You can de-risk it. The classic approach is to just build the thing and find out at the end whether it was worth it. The smarter approach is to identify the riskiest assumptions up front — the leap-of-faith assumptions — and close fast feedback loops on them one at a time, taking the minimum step that answers each question. Every loop either de-risks the idea or tells you to pivot before you have spent much. That is the whole game, and it is what agile is actually for: agile is risk-driven development. It does not eliminate risk. It lets you surf it efficiently and capture the alpha.

Value and risk travel together

Start with something everyone has thought about: a pension fund. If you want it to really grow, you have options, and they line up on a clear gradient. Leave the money in a government-backed account and you have essentially zero risk and essentially zero growth. Move to bonds and you have low risk and modest growth. Move into stocks and the potential value rises — but so does the risk. Even within stocks there is a gradient: an index fund gives you market returns at lower risk, while betting everything on one name — NVIDIA, Tesla, whatever the story stock of the moment is — carries far more risk for a shot at far more return. Investors have a word for the return above the market: alpha. And alpha comes with risk. You do not get one without the other.

This is not a quirk of investing. It is everywhere. A corporate job is lower-risk than becoming an entrepreneur — and lower potential value, because a safe corporate job does not come with the chance of an exit. Joining a startup as an early employee rather than a founder puts you somewhere in the middle. Starting something new has enormous upside, and most of those ventures fail. The same gradient runs straight through product development. Build something that is not really new and the risk is low, but the value will not be there. Reach for a genuinely unique value proposition and the value is real — and so is the risk. That is the alpha of product development, and it is true right down to the level of individual features you choose to fund.

The trap of risk aversion

Once you see the gradient, the obvious mistake is to chase the high-value, high-risk corner blindly. Do not do that — do not pour effort into things that carry a lot of risk without much potential value, and do not skip the cheap wins. There are situations where you genuinely can find a lot of value without much risk: an established product whose customers are clearly telling you exactly what they need. When that happens, go build it; do not over-think it.

But the more common and more dangerous failure is the opposite one. A lot of organizations get stuck in the low-risk, low-value corner — in their product development and in how they run the business as a whole. The reason is rarely a considered strategy. It is the incentive structure. In many organizations it becomes politically dangerous to own anything with real potential value, precisely because of the risk attached to it. So capable people quietly steer toward the safe corner, and the organization slowly optimizes itself into low returns. There is not much risk there. There is not much future there either.

You can de-risk what you cannot eliminate

Here is what makes product and business risk different from a stock pick: you can actually do something about it. Unlike the stock exchange, where you place your bet and ride the outcome, an initiative’s risk can be reduced over its lifetime.

Think about the shape of a high-value, high-risk initiative over time. You start with a lot of risk. If you believe that risk is worth carrying because the potential value is high, then the job from that point on is to learn and de-risk as efficiently as possible. The classic way to execute is to just go do it — build, build, build — and only discover at the end whether it was worth doing. The smarter way is to de-risk along the way: look at what the actual risks in the idea are, and close feedback loops on those risks as quickly as you can.

Concretely, that means identifying the assumptions the whole thing rests on — the leap-of-faith assumptions — and then building a plan that learns on them one at a time, in the order of how much they threaten the initiative.

A razor, and its leap-of-faith assumptions

Make it concrete with a product. Say you have an idea for a new men’s grooming razor. Two things are new about it. One is a magnetic base, so it sits cleanly on the bathroom counter. The other is a feature that goes beyond shaving and is supposed to deliver some additional benefit — and there is a real open question about that benefit. Is it actually valuable? The assumptions stack up fast: Will consumers even notice the new feature? Once they notice it, will they like it? Will they find it delightful? Will they pay for it?

Those are all good questions, and naming them is the move. Once you have them, you build a plan that learns on them as quickly as possible — instead of spending months building the thing, designing the packaging, and figuring out the marketing before you know whether the core bet holds. You cannot test every assumption at once, so you sequence them: each step is the minimum step that answers the next question.

Maybe you make a prototype and hand it to some consumers: do you notice any difference between this version and that one? If nobody notices anything, you have just learned the difference is a real risk — and you go back to the drawing board (or the CAD software) and design something more noticeable, more textured, before you waste another month. Then you run it again, and this time consumers do notice. Now you ask the next question: do you like it? You are hoping that, say, five out of ten like the sensation. Maybe the answer is that now they notice it, they do not actually like it — so you change direction.

Every one of those assumptions has two possible outcomes. Either you de-risk — the choice held, people noticed, people liked it — and the initiative carries less risk than it did. Or you learn that you were wrong and need to pivot, having minimized what you spent before finding out. Sometimes invalidating an assumption invalidates the whole idea — and that is still a success, because you only spent a limited amount of money, time, and people to learn it.

Agile is risk-driven development

Step back and look at what that process actually did. You chose a high-potential idea. You identified your biggest leap-of-faith assumptions. You built a backlog of learning steps and worked through them one by one, adding work only where a loop told you something needed fixing. You navigated a path to the value while spending as little as possible on directions that did not pan out. In effect, you kept the high potential value of the idea while pulling its risk profile way down.

That is the honest answer to why organizations invest in agile. Strip away the ceremonies and the vocabulary, and agile is a way to execute in a risk-driven way. Agile is risk-driven development. It applies to new product development, to new features, to strategic business initiatives, to your operating model — even to a career. In every one of those fields there is potential alpha, and that alpha comes bundled with risk. Agility is the discipline that lets you reach for the alpha while efficiently surfing the risk down. You cannot eliminate the risk. You can refuse to discover it the expensive way.

Watch the episode

This article came out of a short solo episode of the podcast, where I sketch the value-versus-risk picture in real time, walk through the razor example, and talk through how de-risking actually plays out over the life of an initiative. If you want the fuller version — including the live drawing of how you pull a high-value, high-risk bet down the risk axis without losing the upside — watch it below.

Prefer audio? Listen on the podcast page or play it on Spotify.

There is no value without risk — not in a pension fund, not in a career, not in a product. The question is never how to avoid the risk. It is how efficiently you can learn your way through it. So: what is the alpha you are tackling with agility?

A free audio series navigating the product operating model landscape — for leaders building modern product-oriented technology organizations.

Yuval Yeret helps product and tech leaders move from agile theater to evidence-informed delivery. Work with Yuval →